All Categories

Featured

Table of Contents

There is no payout if the plan runs out prior to your fatality or you live beyond the policy term. You may have the ability to renew a term plan at expiration, but the premiums will certainly be recalculated based on your age at the time of renewal. Term life insurance policy is typically the the very least pricey life insurance available due to the fact that it offers a survivor benefit for a limited time and doesn't have a cash money worth component like permanent insurance coverage.

At age 50, the costs would climb to $67 a month. Term Life Insurance Policy Rates thirty years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life policy, for males and females in exceptional health. In contrast, below's a take a look at rates for a $100,000 whole life policy (which is a kind of irreversible plan, indicating it lasts your life time and includes cash money worth).

Rate of interest rates, the financials of the insurance policy business, and state guidelines can additionally impact premiums. When you consider the amount of protection you can obtain for your premium dollars, term life insurance tends to be the least expensive life insurance.

He buys a 10-year, $500,000 term life insurance coverage policy with a premium of $50 per month. If George passes away within the 10-year term, the policy will pay George's recipient $500,000.

If George is diagnosed with an incurable health problem during the first plan term, he probably will not be eligible to renew the plan when it expires. Some policies offer assured re-insurability (without evidence of insurability), yet such functions come at a higher expense. There are several sorts of term life insurance policy.

The majority of term life insurance coverage has a degree costs, and it's the type we've been referring to in many of this short article.

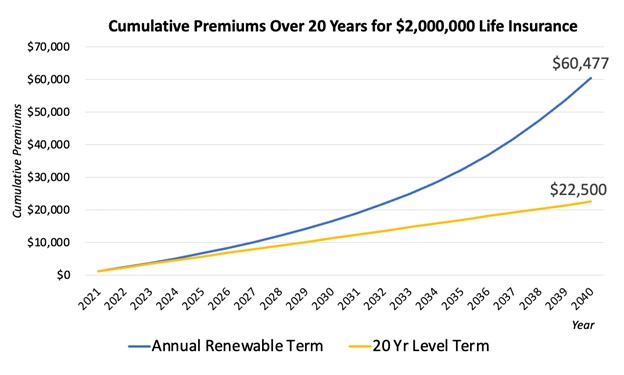

Guaranteed Annual Renewable Term Life Insurance

Term life insurance policy is eye-catching to youths with children. Moms and dads can get considerable protection for an inexpensive, and if the insured dies while the policy holds, the household can count on the survivor benefit to replace lost revenue. These plans are additionally fit for people with expanding families.

The best option for you will depend upon your needs. Below are some points to take into consideration. Term life plans are perfect for individuals who desire significant coverage at a low cost. Individuals who possess entire life insurance pay extra in premiums for much less coverage however have the protection of understanding they are safeguarded permanently.

The conversion biker need to permit you to transform to any long-term plan the insurer provides without limitations. The key functions of the rider are maintaining the initial wellness score of the term policy upon conversion (even if you later on have health problems or come to be uninsurable) and choosing when and exactly how much of the coverage to convert.

Obviously, total premiums will certainly raise dramatically because whole life insurance policy is more pricey than term life insurance policy. The benefit is the ensured authorization without a clinical examination. Clinical problems that create throughout the term life period can not trigger costs to be enhanced. Nevertheless, the firm may call for limited or full underwriting if you want to include additional riders to the brand-new plan, such as a long-lasting treatment rider.

Term life insurance policy is a reasonably cost-effective means to provide a round figure to your dependents if something happens to you. It can be a good choice if you are young and healthy and sustain a family members. Whole life insurance policy comes with substantially greater regular monthly premiums. It is meant to give protection for as long as you live.

Honest A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

It depends upon their age. Insurer set a maximum age limit for term life insurance coverage plans. This is generally 80 to 90 years old however may be higher or lower depending on the business. The premium additionally climbs with age, so a person aged 60 or 70 will certainly pay substantially greater than a person decades more youthful.

Term life is rather comparable to auto insurance. It's statistically unlikely that you'll need it, and the premiums are money down the drain if you do not. If the worst happens, your family will obtain the benefits.

The most popular type is currently 20-year term. The majority of firms will certainly not sell term insurance policy to a candidate for a term that finishes past his or her 80th birthday. If a plan is "sustainable," that means it proceeds effective for an added term or terms, up to a specified age, also if the wellness of the guaranteed (or various other factors) would certainly cause him or her to be turned down if she or he obtained a new life insurance policy plan.

Premiums for 5-year sustainable term can be level for 5 years, then to a new price mirroring the new age of the guaranteed, and so on every five years. Some longer term policies will guarantee that the costs will not boost during the term; others do not make that assurance, making it possible for the insurer to raise the rate throughout the policy's term.

This means that the plan's proprietor can change it right into a long-term type of life insurance policy without added proof of insurability. In a lot of kinds of term insurance, consisting of homeowners and auto insurance, if you have not had a case under the policy by the time it runs out, you get no refund of the premium.

Reliable What Is Direct Term Life Insurance

Some term life insurance customers have actually been unhappy at this end result, so some insurance providers have produced term life with a "return of costs" feature. term 100 life insurance. The premiums for the insurance coverage with this attribute are frequently significantly greater than for policies without it, and they normally require that you keep the policy in force to its term or else you waive the return of costs advantage

Degree term life insurance policy costs and fatality benefits stay constant throughout the plan term. Level term plans can last for periods such as 10, 15, 20 or thirty years. Level term life insurance coverage is normally much more inexpensive as it doesn't construct cash worth. Degree term life insurance policy is one of one of the most usual kinds of security.

What Is Level Term Life Insurance

While the names usually are used interchangeably, degree term coverage has some crucial differences: the premium and death benefit remain the very same throughout of coverage. Degree term is a life insurance policy plan where the life insurance policy costs and survivor benefit stay the exact same for the period of insurance coverage.

{kind=link}

Latest Posts

Final Expense Program

Sell Final Expense Over The Phone

Mutual Of Omaha Final Expense Insurance